Let’s be honest for a moment. When you finally got the keys to your home, insurance was probably the absolute last thing on your mind. You were too busy measuring the living room for that perfect sofa, worrying about painting budgets, or figuring out how to get the local internet provider to install a connection that actually works. Buying a house is an emotional rollercoaster, and wrapping your head around a 50-page insurance policy feels like reading tax law in ancient Sanskrit.

But here’s the thing: your home is likely the single biggest financial investment you will ever make. And yet, so many of us treat our insurance like a checkbox on a bank’s mortgage requirement form. We sign it, tuck it away in a drawer, and hope we never have to think about it again. That is, until a massive storm hits, a pipe bursts on the top floor, or a fire damages the kitchen, leaving us stranded. If you want to avoid a heartbreaking financial disaster, you need to understand how the system works. Today, let’s break down the essential Home Insurance Tips Every Homeowner Should Know so you can protect your sanctuary without losing your sanity.

The Uncomfortable Truth About Replacement Cost vs. Market Value

When I first bought a property, I made a massive assumption. I thought, “Okay, if my house is worth 1.5 crores on the open market, I should insure it for 1.5 crores, right?” Wrong. This is the single most common trap homeowners fall into, and it can cost you dearly when you make home insurance claims down the road.

Your home’s market value includes the price of the land it stands on. But unless a meteor strikes, the land isn’t going anywhere. If your house burns down, you don’t need to buy new land; you just need to rebuild the structure. Therefore, your home insurance policy should be based on the replacement cost value of the building, not its market value. The replacement cost is what it would actually cost to clear the debris and rebuild your home from scratch, using modern materials and hiring local labor at today’s prices.

Conversely, some homeowners make the opposite mistake. They underinsure their home to save on premiums, thinking, “A total loss will never happen to me.” If you insure your home for only 50% of its actual rebuilding cost, your insurer might apply what is known as the “average clause” during a claim. That means if you suffer minor property damage that costs 10 lakhs to fix, the insurer might only pay out 5 lakhs because you were underinsured. It’s a harsh reality, but understanding this distinction is the foundation of any smart insurance strategy.

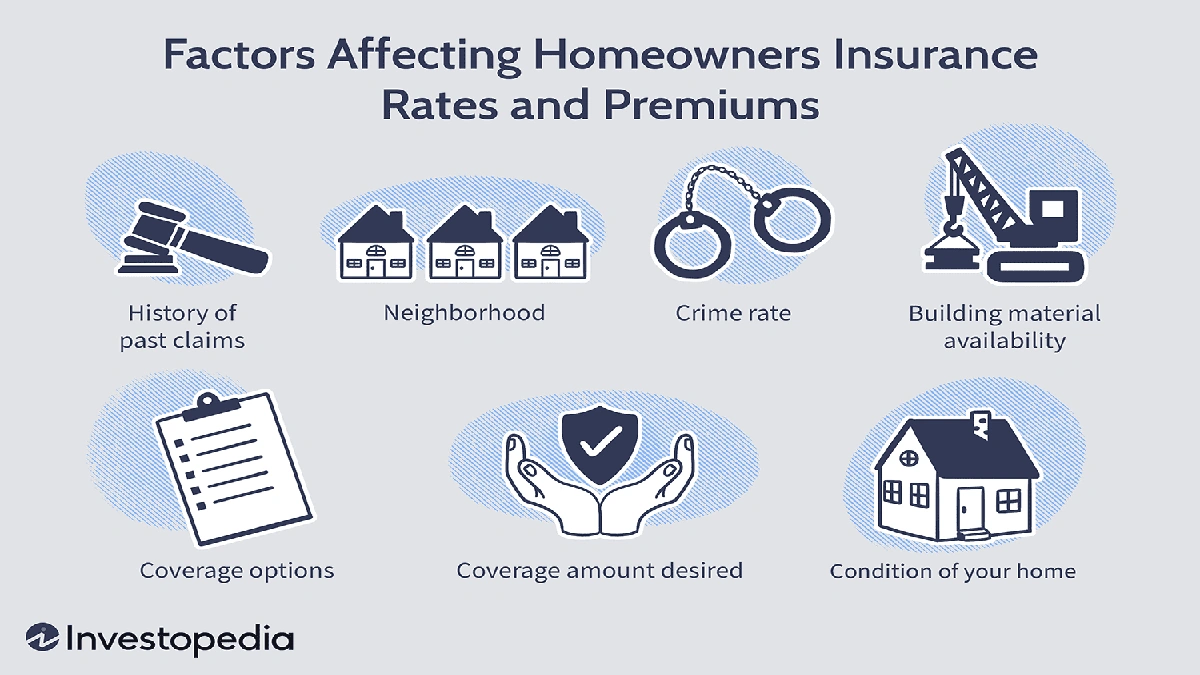

Decoding the Core Pillars of Your Coverage

Insurance policies are notorious for using jargon that makes your eyes glaze over. Let’s strip away the corporate speak and look at what actually matters. A standard comprehensive policy is usually divided into a few core sections, and you need to customize each of them:

- Dwelling Coverage: This is the backbone of your policy. It covers the physical structure of your house—the walls, the roof, the floors, and built-in fixtures. When calculating your dwelling coverage, make sure to account for any unique architectural features or high-end finishes you’ve added.

- Personal Property Coverage: This covers everything inside your home—your furniture, electronics, clothes, and appliances. A quick pro-tip: do a quick walk-through of your house with your smartphone and record a video of every room, opening closets and drawers. This digital inventory is invaluable if you ever need to file a claim.

- Liability Coverage: This is the part people ignore until it’s too late. What happens if a delivery person slips on your wet driveway and breaks their wrist? Or if your dog slips out of the gate and bites a neighbor? Without adequate liability coverage, you could be personally sued for medical bills and legal fees, which can easily wipe out your savings.

If you’re managing multiple properties or dealing with complex real estate assets, staying organized is key. Some modern property managers even use specialized digital tools to keep track of their portfolios. For instance, if you are overseas or managing UK assets, checking out a CRM for real estate agents in UK can help you see how professionals manage extensive property documentation and insurance deadlines seamlessly.

Deductibles and Discounts | Playing the Premium Game Wisely

We all want to save money, but lowering your insurance premium by slashing your coverage limits is a terrible idea. Instead, you should look at your deductible options . The deductible is the out-of-pocket amount you agree to pay before your insurance policy kicks in.

Think of it this way: if you have a 10,000-rupee deductible and a storm causes 50,000 rupees worth of damage to your roof, you pay the first 10,000, and the insurer pays the remaining 40,000. If you raise your deductible to 25,000 rupees, your monthly or annual premium will drop significantly. Why? Because the insurance company knows you are less likely to file small, pesky claims. It’s a calculated risk, but if you have a solid emergency fund, opting for a higher deductible is one of the easiest ways to keep your premium costs down.

What else can you do? Ask for discounts! Most insurers offer loyalty discounts, claims-free discounts, or safety discounts. If you install a certified security system, smoke detectors, gas leak sensors, or deadbolts on your doors, you are actively reducing the risk of theft and property damage . Make sure your agent knows about these upgrades so they can apply those sweet discounts to your premium. In the digital age, operational efficiency is everything, and insurers love clients who mitigate risks. Just as businesses track top CRM trends in 2026 to optimize their workflows, you should optimize your home’s safety ecosystem to get the best financial rates.

The Dreaded “Excluded Perils” | What Your Policy Won’t Cover

Here is where many homeowners face their biggest shock. They assume that “all-risk” or “comprehensive” means absolutely everything is covered. It doesn’t. In the insurance world, what isn’t covered is often more important than what is.

Standard home policies almost always exclude damage caused by earthquakes, floods, and general wear and tear. If you live in a low-lying area prone to monsoon flooding, or in an active seismic zone, you must purchase specific add-ons or riders to cover these risks. Don’t wait for the clouds to gather to ask your agent about flood coverage; most companies have a 30-day waiting period before a new flood policy becomes active.

Furthermore, regular maintenance issues are entirely your responsibility. If a slow, hidden leak behind your bathroom wall causes wood rot over three years, your insurer will likely reject the claim. They expect you to maintain your home. Insurance is designed for sudden, accidental, and unforeseen disasters not for ignoring a leaky pipe you should have fixed months ago. For more detailed industry regulations, you can check the official guidelines on homeowners insurance basics to understand how global standards shape local policies.

How to Navigate the Claims Process Without Losing Your Mind

When disaster strikes, adrenaline runs high. It’s easy to panic. But the steps you take in the first 48 hours after a loss will determine whether your claim gets approved smoothly or gets bogged down in bureaucratic limbo.

First, mitigate further damage. If a pipe bursts, shut off the main water valve immediately. If a window breaks, board it up. Insurers expect you to take reasonable steps to prevent the damage from getting worse. Next, take photos and videos of everything before you start cleaning up. Do not throw away damaged items until an insurance adjuster has had a chance to inspect them.

When you file, be completely honest and highly detailed. Provide the receipts, photos, and any proof of ownership you have. Keep a log of every conversation you have with your insurance company, noting the date, time, and the name of the representative you spoke with. It sounds tedious, but when you are dealing with large sums of money, paper trails are your best friend.

Frequently Asked Questions

Home Insurance FAQs

Is home insurance legally mandatory in India?

No, home insurance is not legally mandatory by law. However, if you are taking a home loan, almost all banks and financial institutions will make it a mandatory condition of the loan to protect their financial interest in the property.

Does my policy cover my tenant’s personal belongings?

No, your home insurance policy only covers the structure and your personal belongings. If you rent out your property, your tenants must buy their own renter’s insurance policy to protect their clothes, electronics, and furniture.

What is the difference between actual cash value and replacement cost?

Actual cash value calculates the cost to replace your item minus depreciation (wear and tear). Replacement cost pays the actual amount it takes to buy a new, similar item today without deducting anything for its age.

Can I transfer my home insurance if I sell my house?

Yes, you can transfer your home insurance policy to the new owner, but it involves a formal process of documentation and approval from the insurance company to update the policyholder details.

Will my premium increase if I make a single claim?

It depends on the size of the claim and your insurer’s policies. While a minor claim might not increase your premium, you will likely lose your “No Claim Bonus,” which could make your renewal slightly more expensive.

Final Thoughts | Don’t Just Set It and Forget It

At the end of the day, home insurance is not a static product. Your life changes, your home changes, and your policy needs to change with it. Did you recently renovate your kitchen? Did you buy an expensive piece of jewelry or a high-end home theater system? If so, your old policy limits might no longer be enough. Make it a habit to review your coverage once a year during renewal time. Sit down, call your agent, and ask the hard questions. Protecting your home isn’t just about paying a premium; it’s about buying the peace of mind that your family’s safe haven is truly secure, no matter what life throws your way.