Imagine this: You have finally found the perfect apartment in Bengaluru, or maybe you are planning to buy that dream car before the festive season. You have done the math, sorted your down payment, and filled out the forms. Then, the dread hits. You get a polite but firm rejection email. The reason? That pesky three-digit number we all ignore until we absolutely cannot: your CIBIL score .

Let’s be honest. Most financial advice on how to improve your credit score fast is painfully boring. It is usually written by people who have never had to scramble to fix a ruined credit history. I have been there. Years ago, my score was sitting at a miserable 610 because of some stupid mistakes in my early twenties. Today, it stands proud at 795. I did not use any shady credit repair agencies; I just cracked the code of how Indian credit bureaus actually calculate your score.

If you are looking to unlock premium credit cards, qualify for lower interest rates, or even secure one of the highest paying entry level jobs without a degree that require background credit checks, you need to fix this now. Grab a cup of chai, and let us dive into the actual step-by-step strategy to make your credit score skyrocket.

The Hidden Culprits Eating Away at Your Score

Before you can fix something, you need to know what is broken. Most people assume that as long as they pay their Minimum Amount Due (MAD) on their credit card, their score will remain healthy. That is a massive myth. In fact, paying only the minimum is a fast track to financial quicksand.

Your credit profile is managed by bureaus like TransUnion CIBIL, Experian, and Equifax. When a bank looks at your loan application , they fetch your credit report from these agencies. But what if that report is flat-out wrong? You would be surprised at how often clerical errors happen. A loan you closed months ago might still show as “active” or “written off,” dragging your score down through no fault of your own.

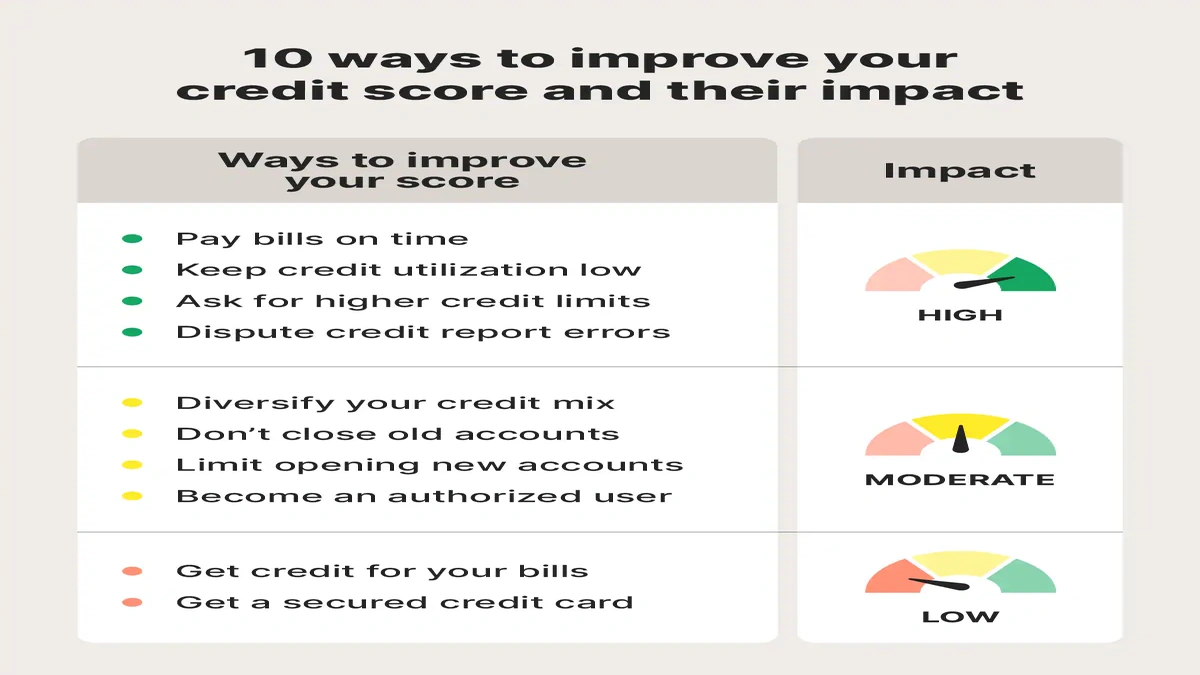

To start your `CIBIL score improvement` journey, you must get your hands on your official report. By law, you are entitled to one free check per year from each bureau. You can easily do this via the official CIBIL website . Once you have it, look for `credit report errors` like misreported delayed payments, incorrect personal details, or duplicate accounts. Finding and disputing even a single mistake can boost your score by 50 to 100 points in less than a month!

The 30-Day Credit Fast-Track Action Plan

If you need quick results, you cannot afford to wait around. You have to take aggressive, tactical actions that force the algorithm to recalculate your risk profile in your favor. Here are the three most powerful levers you can pull right now.

1. Smash Your Credit Utilization Ratio

What is your `credit utilization ratio`? Simply put, it is how much of your available credit card limit you actually use. If your total limit across all cards is ₹1,00,000 and you spend ₹90,000, your utilization is 90%. To the algorithms, you look “credit-hungry” and desperate.

The golden rule is to keep your credit utilization under 30%. If you want to raise your score fast, try prepaying your bill before the official statement generation date. When the bank reports your data to the bureau at the end of the month, they will report a super-low balance, instantly boosting your score.

2. Automate Every Single Credit Card Payment

Your payment history accounts for a whopping 35% of your total score. A single missed credit card payment can linger on your history like a bad smell for up to seven years. It is brutal. The easiest way to bypass human forgetfulness is to set up an auto-debit for the “Total Amount Due” (never the minimum amount).

If your finances are currently tight, learning to create a monthly budget that works is your absolute best defense. Align your payment dates to fall right after your salary hits your account so you are never caught empty-handed.

3. Diversify Your Credit Mix

Lenders love stability. If you only have credit cards (unsecured credit), you might look a bit risky. Having a balanced credit mix of secured loans (like a car loan or home loan) and unsecured credit shows that you can handle different types of financial responsibilities. If you only have unsecured debt, do not rush to take an unnecessary loan, but keep this balance in mind for the future.

The Clever Hacks for Credit Beginners

But what if you have no score at all? Or what if your score is so bad that no bank will issue you a standard credit card? This is a classic catch-22: you need credit to build credit, but you cannot get credit without a score.

This is where `secured credit cards India` come to the rescue. Almost every major Indian bank offers these cards against a Fixed Deposit (FD). You open an FD of, say, ₹20,000, and the bank issues you a credit card with a limit of 80-90% of that deposit. Because the bank has zero risk, they will approve it instantly no income proof or past score required. Use this card to buy groceries, pay your utility bills, settle the balance in full every month, and watch your credit footprint grow from scratch.

Another crucial factor is your `credit history age`. Do not close your oldest credit card accounts, even if you do not use them anymore. The length of time you have successfully managed credit matters. Keeping that old college credit card active shows lenders you have a long, trustworthy relationship with credit.

What to Avoid | The Desperation Pitfalls

When people are desperate to fix their credit, they often make moves that make them look incredibly risky to banks. Let me save you from these self-inflicted wounds:

- Stop applying for multiple credit cards at once: Every time you apply, the bank makes a “hard inquiry” on your report. Multiple hard inquiries within a short period scream financial distress.

- Avoid settling loans for less than the due amount: If a bank offers you a “One-Time Settlement” to close a debt, run away. It will be reported as “Settled” rather than “Closed,” which ruins your chances of getting a loan for years.

- Do not ignore your co-signer responsibilities: If you co-signed a loan for a friend or relative and they miss a payment, it hurts your score just as much as theirs. Keep track of those payments!

Frequently Asked Questions

How to Fix Your Credit Score Fast

Can I raise my credit score by 100 points in 30 days?

It is highly possible if your low score is due to high credit card utilization or easily fixable errors on your report. Paying down your balances to under 10% and successfully disputing incorrect entries can result in a rapid, dramatic jump within a single billing cycle.

Does checking my own score lower it?

No, not at all! When you check your own score, it is considered a “soft inquiry” and has absolutely zero impact on your rating. Only “hard inquiries” initiated by lenders when you apply for new loans or cards will affect your score.

What is a good CIBIL score to target for easy loan approvals?

In India, any score above 750 is considered excellent. It gives you the maximum leverage to negotiate lower interest rates on home loans and secure premium credit cards with great travel and cashback perks.

How long do negative remarks stay on my CIBIL report?

Generally, negative remarks, missed payments, and defaulted accounts stay on your credit history for up to seven years. However, their impact on your score diminishes over time as you build a fresh record of positive, timely payments.

The Final Word

Improving your credit score is not about a sudden, dramatic stroke of luck. It is about small, deliberate habits. It is about checking your report for errors, keeping your spending in check, and paying your dues on time, every single time. Treat your credit score like a financial mirror it simply reflects your daily habits back at you. Start taking control of it today, and watch your financial doors swing wide open.