Let’s be honest. We’ve all been there. It is late at night, you are staring at your laptop screen, and a sudden, unexpected financial emergency is staring right back at you. Maybe it is a medical bill, a sudden car repair, or an urgent home renovation before the monsoons hit. You decide to apply for a loan, feeling relatively confident, only to get hit by that cold, automated rejection email. The culprit? A three-digit number that suddenly feels like a life sentence: your credit score.

If you are dealing with a poor CIBIL score, the mainstream financial world can feel incredibly hostile. Major banks turn a blind eye, leaving you wondering if there are any genuine low credit score loan options left. But here is the thing you are not out of options. While it is true that a low score makes things harder, getting one of the best personal loans for bad credit scores is not impossible. It just requires a different strategy. Let’s sit down, grab a cup of coffee, and unpack exactly how you can navigate this tricky landscape without falling into predatory debt traps.

The Cold Truth About Your CIBIL Score (And Why It’s Not the End of the Road)

Before we dive into the solutions, we need to understand the battlefield. In India, most traditional banks treat your CIBIL score as the ultimate gatekeeper. If your score is below 650, you are instantly flagged as “high risk.” But why does this happen? Usually, a low score is the result of a bad credit score history , which might include past missed EMIs, credit card defaults, or simply having a “thin” credit file because you have never borrowed money before. Ironically, not borrowing money can sometimes hurt you just as much as borrowing too much.

However, what traditional banks fail to see is the human story behind those numbers. You might have missed payments during a tough phase, like a job transition or a medical crisis, but your current income might be perfectly stable. Thankfully, newer digital lenders and alternative platforms look beyond just your past mistakes. They are more interested in your present repayment capacity. But before you dive headfirst into borrowing, understandinghow personal loans workis crucial so you don’t end up in an even deeper financial hole.

The Best Personal Loans for Bad Credit Scores | Your Actionable Roadmap

So, how do you actually get cash in your bank account when your credit history is less than stellar? Here are the most viable paths available in India right now, ranked by their feasibility and safety.

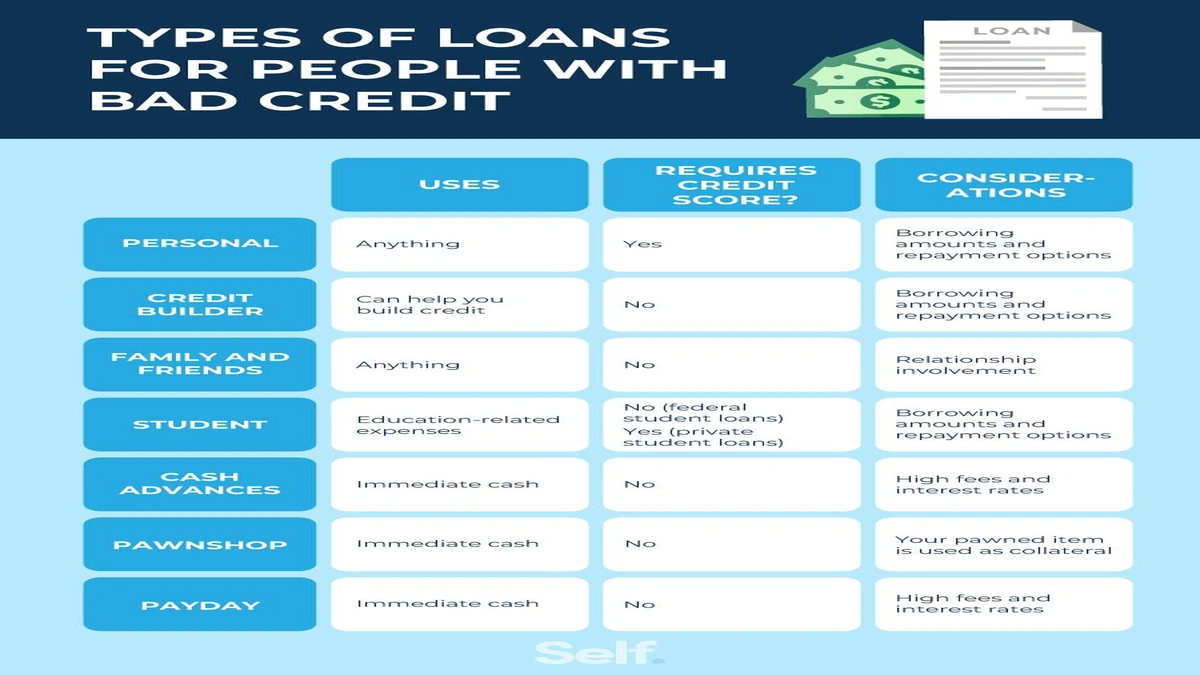

1. Fintech NBFCs and Specialized Digital Lenders

The rise of financial technology has changed the game. Many non-banking financial companies (NBFCs) now offer instant personal loan apps in India that use advanced algorithms to assess your creditworthiness. Instead of just looking at your CIBIL report, they analyze your monthly bank statements, utilities payment history, and even your employment stability.

While these lenders might offer bad credit personal loans , you must brace yourself for higher interest rates. Because they are taking a bigger gamble on you, the interest rates on personal loans from these platforms can range anywhere from 24% to 36% per annum. It is expensive, yes, but if you need urgent liquidity, it is a highly accessible option.

2. Peer-to-Peer (P2P) Lending Platforms

If traditional banks say no, why not borrow directly from individual investors? This is exactly what peer to peer lending platforms do. These platforms act as matchmaking portals, connecting individuals who need money with investors looking to earn a higher return than a typical fixed deposit. On a P2P platform, you are treated as an individual, not just a score. You can explain your situation, show your current income proof, and get funded by multiple small investors who believe in your story.

3. Secured Loans | The Ultimate Credit Score Bypass

If you have some form of asset, you can completely bypass your bad credit score. This is arguably the safest and cheapest way to get a loan when your credit is low.

- Secured Loan against FD: If you have a fixed deposit, you can easily get a secured loan against FD. Banks will typically lend you up to 90% of your FD value. The interest rate is incredibly low—usually just 1% to 2% higher than what your FD is earning—and your credit score is completely ignored.

- Gold Loans: In India, gold is not just an ornament; it is financial security. You can walk into almost any bank or gold loan company, hand over your gold, and walk out with cash in under an hour. No credit checks, no endless paperwork.

4. Apply with a Co-Applicant

If your credit history is holding you back, you can lean on someone else’s good financial standing. Applying for a co-applicant personal loan with a spouse, parent, or sibling who has a high credit score and a stable income can dramatically increase your approval chances. This reassures the lender that if you fail to repay, the co-signer will step up to cover the debt.

How to Protect Yourself from Predatory Loan Apps

I need to pause here and give you a serious warning. The digital loan space in India has a dark side. There are dozens of illegal, fraudulent loan apps operating on the fringes of the internet. They promise instant loans without any credit checks, but once you download their app, they harvest your contacts and use aggressive, highly unethical recovery tactics.

Always verify that any lender you deal with is officially registered with theReserve Bank of India(RBI). If an app demands upfront processing fees before disbursing the loan, or asks for access to your entire contact list, close the app immediately. No legitimate lender operates this way.

Your Long-Term Strategy | Turning Bad Credit into Good Credit

Getting a loan to solve a current crisis is a short-term fix. Your ultimate goal must be CIBIL score improvement . Think of your bad credit loan not just as an expense, but as an opportunity. If you pay your new loan EMIs strictly on time, your credit score will naturally start to climb. Within six to twelve months, you will see your score move from the red zone to the green zone.

Managing your money during these times is also about maintaining sanity through financial stress. Just like nourishing your brain with thebest foods for brain healthkeeps you mentally sharp, keeping your finances organized reduces cognitive overload and helps you make rational, stress-free decisions.

Start by downloading your official report directly from theofficial CIBIL website. Check for any errors, clear off any tiny outstanding credit card dues, and promise yourself that you will never miss an EMI deadline again. Your future self will thank you.

Frequently Asked Questions

Can I get a personal loan if my CIBIL score is below 500?

Yes, but traditional banks will almost certainly reject you. Your best options are secured loans (like gold loans or loans against fixed deposits) or peer-to-peer (P2P) lending platforms that evaluate your current income rather than just your past credit history.

Are the interest rates higher for bad credit personal loans?

Absolutely. Lenders view a low credit score as a high risk. To compensate for this risk, they charge significantly higher interest rates, which can range from 18% to over 35% per annum depending on the lender.

How long does it take to rebuild a bad credit score?

Rebuilding a credit score is a slow process. It usually takes about 6 to 12 months of consistent, on-time payments of your EMIs and credit card bills to see a substantial improvement in your CIBIL score.

Should I use an instant mobile app to get a loan with bad credit?

Only use apps that are officially partnered with RBI-registered NBFCs or banks. Avoid unregulated apps that promise overnight loans with no documentation, as they are often predatory and illegal.

Can a co-applicant help me get a lower interest rate?

Yes, applying with a co-applicant who has an excellent credit score and a stable income can help you get approved faster and may also help you negotiate a lower interest rate with the lender.