Picture this: You are sitting in your favorite local coffee shop in Mumbai, sipping on a warm cutting chai, when your phone buzzes. It is a text message from your bank, glowing with promise: “Good news! You have a pre-approved personal loan of ₹5,00,000 waiting in your account. Click here to disburse instantly!”

It feels like magic, doesn’t it? In a world where immediate gratification is just a tap away, the temptation to click that link is incredibly real. But here is the thing we rarely talk about over coffee: that instant money isn’t a gift. It is a financial tool one that can either build your dream or quietly dismantle your financial peace of mind. To master your money, you must understand exactly How Personal Loans Work and When to Use Them before you sign on the dotted line.

Let’s lift the curtain on how these loans actually function, expose the hidden traps, and pinpoint exactly when you should say yes and more importantly, when you should run in the opposite direction.

The Core Mechanics | What Happens When You Borrow?

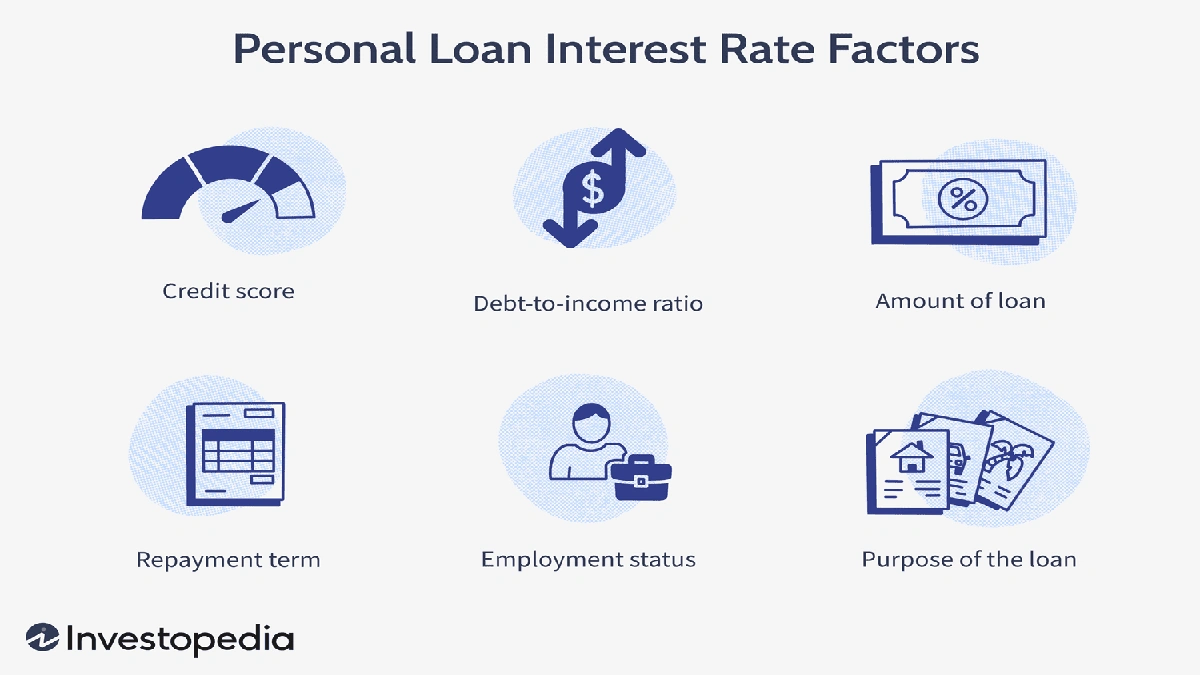

At its most basic level, a personal loan is an unsecured personal loan . Unlike a home loan or a car loan, where the bank can seize your property if you stop paying, a personal loan requires no collateral. You don’t have to pledge your gold, your house, or your mutual fund portfolio to get the cash.

But let’s be honest: banks are not in the business of charity. Because they are taking a higher risk by lending you money without any security, they protect themselves in two primary ways: your credit history and the interest rate. According to the foundational definitions of unsecured debt structures , lenders charge higher premiums precisely because they have no physical asset to fall back on if a borrower defaults.

This is where your credit score comes into play. In India, your CIBIL score is essentially your financial report card. If you have a score above 750, banks view you as a reliable friend and will offer you competitive personal loan interest rates . If your score is lagging in the 600s, you will either face outright rejection or be hit with astronomical interest rates that make borrowing incredibly expensive.

When you are approved, the bank gives you a lump sum of money, which you agree to pay back in fixed monthly installments (EMIs) over a specific repayment tenure , usually ranging from 12 to 60 months. It sounds straightforward, but the devil is always in the mathematical details.

The Math Traps | Reducing vs. Flat Interest Rates

Here is a secret that many bank agents won’t openly explain unless you ask them directly. There are two ways lenders calculate interest: the flat rate and the reducing balance rate. Understanding the difference can save you thousands of rupees.

With a flat interest rate, the interest is calculated on the entire initial loan amount throughout the entire tenure. So, even if you have paid off 80% of your loan, you are still paying interest on the full amount you borrowed on day one. On the other hand, a reducing balance rate calculates interest only on the remaining outstanding principal. Always, without exception, insist on a reducing balance calculation. It is mathematically far friendlier to your wallet.

Additionally, you must look out for the sneaky upfront costs. Many borrowers look only at the monthly EMI and completely ignore the processing fees . This fee, which typically ranges from 1% to 3% of the total loan amount, is deducted before the money even hits your bank account. If you borrow ₹2,00,000 with a 3% processing fee, you will only receive ₹1,94,000, yet you will still owe interest on the full ₹2,00,000. It is a small detail, but a crucial one when you are calculating the real cost of your debt.

When to Say Yes | The Smart Ways to Use a Personal Loan

Now that we know how the machinery works, let’s talk strategy. A personal loan is a high-cost tool, which means it should only be used for high-value financial moves. Here are the few scenarios where taking out a loan actually makes perfect sense.

1. High-Interest Debt Consolidation

If you are juggling multiple credit cards, you are likely paying interest rates as high as 36% to 42% per annum. This is a financial emergency. Using a personal loan at 11% or 12% for debt consolidation to pay off those credit cards is a brilliant move. You instantly lower your interest cost, simplify your life into a single monthly payment, and give yourself a realistic timeline to become debt-free.

2. Medical Emergencies and Unplanned Healthcare Costs

Life has a habit of throwing curveballs when your emergency fund is low. Whether it is an unexpected medical emergency or a critical procedure highlighted in a comprehensive dental health guide on oral hygiene , cash flow shortages are real. While health insurance is your first line of defense, a personal loan can act as a reliable financial bridge to cover immediate hospital deposits, treatments, or specialized dental surgeries that insurance might not cover.

3. Investing in Your Career or High-ROI Upgrades

Borrowing to invest in yourself is often a smart move. If you need a specialized certification to double your salary, or if you need to upgrade your professional equipment to scale your freelance business, a loan can be justified. However, you must treat your personal life like a business. Just as an enterprise figures out how to calculate ROI of CRM software before investing in expensive tools, you should calculate the return on investment of your loan. If the interest cost of your loan is 12%, but the skill upgrade increases your earning potential by 40%, the math works heavily in your favor.

When to Walk Away | The Financial Red Flags

Let’s be completely honest with each other: using a personal loan to fund lifestyle choices is a recipe for long-term stress. If you are tempted to apply for a pre-approved personal loan to buy the latest flagship smartphone, host a lavish destination wedding, or fund a luxury holiday in Europe, stop and close the app.

The dopamine hit of a new gadget or a beautiful vacation fades within a few weeks. The monthly EMIs, however, will stick around for the next three to five years, eating into your monthly savings and preventing you from building real wealth. If you cannot afford to buy a consumer luxury with your cash, you certainly cannot afford to buy it with someone else’s expensive money.

As you map out your long-term financial planning , remember that debt is a claim on your future time and labor. Every EMI you commit to means you have to work that much harder tomorrow just to stay even. Use credit to build your future, not to subsidize a lifestyle you haven’t earned yet.

Frequently Asked Questions

How does my credit score affect my personal loan interest rate?

Your credit score is the primary metric lenders use to gauge your risk. A high score (above 750) signals that you manage debt responsibly, allowing you to qualify for the lowest available interest rates. A lower score indicates higher risk, which means lenders will either charge you a much higher interest rate to offset that risk or reject your application entirely.

Can I pay off my personal loan early to save on interest?

Yes, most banks allow foreclosure or part-payments, but they often charge a prepayment penalty, which can range from 2% to 5% of the outstanding principal balance. Always read your loan agreement’s fine print to ensure the interest savings from paying early outweigh the prepayment fees.

What is the difference between a secured loan and an unsecured personal loan?

A secured loan requires you to pledge an asset like a house, car, or gold as collateral. If you default, the bank can sell that asset to recover their money. An unsecured personal loan requires no collateral, relying solely on your creditworthiness and income stream, which is why it typically carries a higher interest rate.

How long does it take for a personal loan to get disbursed?

For pre-approved offers, disbursement can happen within minutes or even seconds via digital banking channels. For standard applications requiring manual income verification and document checks, the process usually takes between 2 to 7 business days.

Should I choose a longer repayment tenure to keep my EMIs low?

While a longer tenure reduces your monthly EMI, it significantly increases the total interest you pay over the life of the loan. It is usually best to choose the shortest tenure with an EMI you can comfortably afford to minimize your overall interest burden.

The Final Verdict

At the end of the day, a personal loan is neither inherently good nor bad; it is simply a tool. If you use it to consolidate toxic credit card debt or to invest in high-yield personal growth, it can be a massive stepping stone. If you use it to fund instant gratification, it becomes a financial anchor. The next time a tempting loan offer pops up on your phone screen, take a deep breath, buy a coffee instead, and make sure you are borrowing with a clear, calculated plan.