Imagine this: You’re sitting in a bustling café in Bengaluru, sipping on a hot filter coffee, trying to make sense of your new insurance policy. You open the PDF, scroll past pages of legal jargon, and boom there it is. The word “deductible” staring back at you. If you’re like most people, your eyes probably glazed over, you closed the tab, and decided to think about it “later.”

But here’s the thing: avoiding this word can cost you thousands, if not lakhs, of rupees. Let’s be honest, insurance companies love confusing us with complex terminology. Today, let’s break down exactly What Is Deductible in Insurance Explained in plain, simple English, so you never overpay for a policy again.

The Coffee-Shop Breakdown | What Actually is a Deductible?

Let’s start with a simple, real-world scenario. Think of a deductible as your “skin in the game.” It is the initial amount of money you agree to pay out of your own pocket before your insurance company steps in to pay the rest of the claim.

To understand the basic insurance deductible definition , think of it as a financial partnership. The insurer is saying, “Look, we’ve got your back for the big disasters, but you need to handle the small bumps yourself.”

So, how insurance deductibles work in practice? Let’s say you have a health policy with a deductible of ₹15,000. If you get admitted to the hospital and the bill comes to ₹50,000, you will pay the first ₹15,000 yourself. The insurance company will then cover the remaining ₹35,000. If your hospital bill is only ₹10,000, you pay the whole thing because it hasn’t crossed your deductible limit. Simple, right?

What fascinates me is how many people assume that having insurance means zero out-of-pocket costs from day one. That misunderstanding is exactly how people end up feeling cheated when filing a claim. Knowing how deductibles work is your shield against these unexpected financial shocks.

The Great Indian Dilemma | Car Insurance Deductibles Decoded

If you own a car in India, you’ve definitely encountered two terms: compulsory and voluntary deductibles. Let’s demystify these because they directly impact your wallet every single year.

First, there is the compulsory deductible in car insurance . As the name suggests, this is mandatory. Set by the Insurance Regulatory and Development Authority of India (IRDAI), this is a fixed amount usually around ₹1,000 to ₹2,000 depending on your engine capacity that you must pay on every single claim. There is no escaping this one.

But then comes the interesting part: the voluntary deductible . This is where you get to play strategist. This is an additional amount you voluntarily agree to pay in case of an accident, in exchange for a massive discount on your own-damage premium.

I initially thought this was a brilliant way to save money on premium costs, but then I realized the catch. If you opt for a high voluntary deductible in car insurance to save ₹2,000 on your yearly premium, but then end up in a minor fender bender, you might have to pay ₹15,000 out of your pocket before the insurer pays a single paisa. It’s a calculated gamble. If you are an incredibly safe driver who rarely takes the car out, go high. If you navigate crazy city traffic daily, keep it low.

Dealing with the stress of car accidents or unexpected financial dents can really take a toll on your peace of mind. If you find yourself constantly worrying about these unexpected life events, taking a moment to breathe and looking intonatural remedies for anxietymight help you manage that daily stress while we figure out the rest of your financial planning.

Health Insurance | Deductibles, Co-payments, and the Fine Print

Now, let’s talk about health insurance deductibles , which operate a bit differently than vehicle ones. In health insurance, a deductible can apply to individual claims or be an annual aggregate.

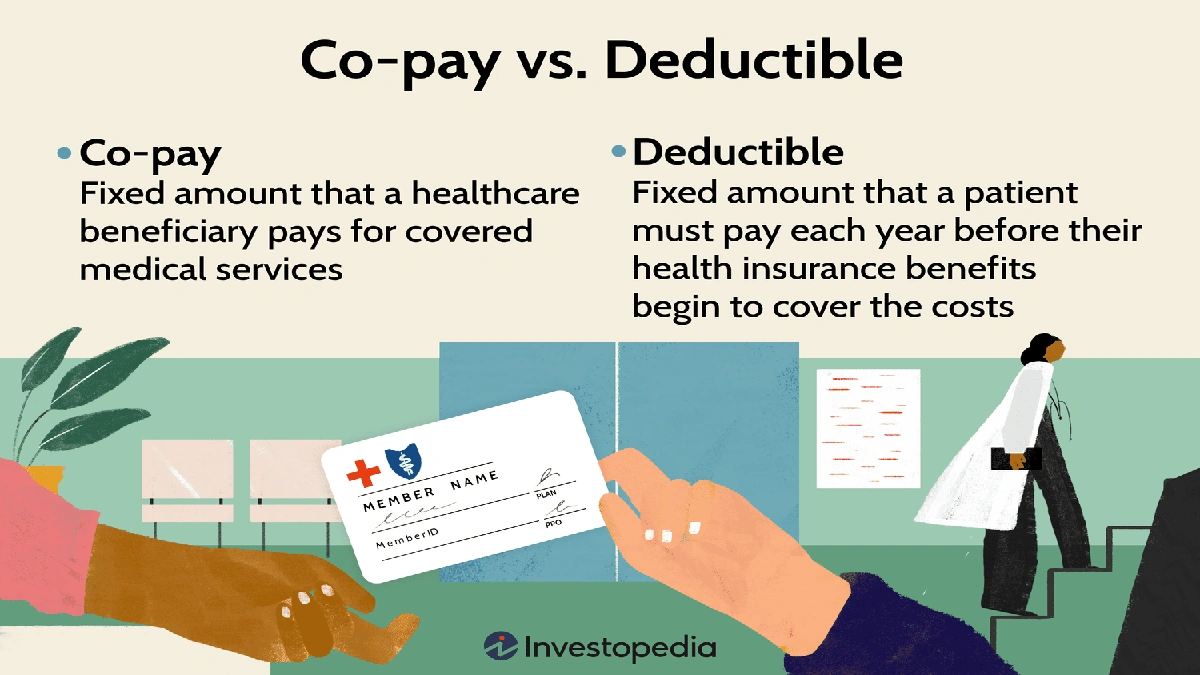

Many people get confused between a co-payment vs deductible . Let’s clear that up once and for all. A deductible is a fixed amount you pay before the insurer pays anything. A co-payment, on the other hand, is a pre-defined percentage of the total claim amount that you agree to pay every single time. For instance, a 10% co-payment on a ₹1,00,000 bill means you pay ₹10,000, and the insurer pays ₹90,000, regardless of any deductibles.

In some markets, you might choose a high deductible health plan (often paired with tax-saving accounts), which offers very low premiums but requires you to cover significant initial healthcare costs. In India, we frequently see this concept applied through ‘Top-up’ or ‘Super Top-up’ policies. These plans only kick in after your primary insurance (or your own pocket) covers a base deductible amount. It’s an incredibly smart, cost-effective way to get high-value health cover.

Of course, health issues aren’t just financial hurdles; they are deeply physical. If you or a family member are managing ongoing physical health struggles alongside navigating insurance, like recovering from an injury or dealing with chronic pain, check out this guide onchronic back pain reliefto help ease the physical burden while you sort out the paperwork.

The Golden Rule | How to Choose Your Deductible Like a Pro

So, how do you actually go about choosing an insurance deductible that fits your life?

Here is my simple, battle-tested formula:

- Check your emergency fund: If you have a solid emergency fund sitting in a savings account, you can comfortably opt for a higher deductible. Why? Because you can easily afford the temporary out-of-pocket hit in exchange for paying much lower premiums month after month.

- Analyze your history: Are you prone to minor claims? If you’re renting a house or driving a car in a high-risk area, a lower deductible is your friend.

- Do the math: Calculate the annual premium savings of a higher deductible. If raising your deductible from ₹5,000 to ₹15,000 only saves you ₹500 a year in premiums, it’s probably not worth the risk. But if it saves you ₹3,000 a year, and you go three years without a claim, you’ve already won.

For more official guidelines and safety regulations on how these terms are structured in consumer contracts, you can always refer to resources like theDeductible Wikipedia pageto understand global standards.

Frequently Asked Questions

What happens if my claim is less than the deductible?

If your claim amount is lower than your agreed deductible, your insurance company will not pay anything. You will have to cover the entire cost yourself, and in most cases, you shouldn’t even bother filing a claim as it might affect your no-claim bonuses.

Do I have to pay my deductible every single year?

In health insurance, yes, deductibles are typically annual, meaning they reset at the beginning of each policy year. For car insurance, however, deductibles apply to every individual claim you file, not on a yearly basis.

Why do insurance companies even have deductibles?

Deductibles exist to prevent people from filing tiny, trivial claims (like a tiny scratch on a car door) that cost the insurance company more in administrative paperwork than the repair itself. It keeps overall premium rates lower for everyone.

Does a higher deductible always lower my premium?

Yes, almost always. By opting for a higher deductible, you are shifting some of the financial risk from the insurer to yourself. Because the insurance company has less potential liability, they reward you with a lower premium rate.

A Final, Powerful Insight

At the end of the day, insurance isn’t about finding a magic policy where you pay absolutely nothing during a crisis. It’s about managing risk. A deductible is not a hidden penalty; it is a leverage tool. Once you understand how to slide that deductible scale up or down based on your personal savings, you stop being a passive consumer and start playing the game like a seasoned financial analyst. Spend an extra ten minutes on your next renewal, do the math, and make your money work for you.