Imagine this: You are sitting in your favorite local coffee shop, sipping a warm cutting chai, and scrolling through home listings on your phone. You spot it the perfect house. The listing price seems within reach, and you feel that sudden surge of excitement. But then, you glance at the current market trends and notice that interest rates have ticked up by just 1%. “No big deal,” you think. “It is just a single percentage point!”

Well, let us be honest. That “tiny” 1% difference is the ultimate financial illusion. It is a quiet domino that, when tipped, can radically alter your monthly budget, determine how much house you can actually afford, and cost you a small fortune over the lifespan of your loan. If you have ever wondered exactly How Mortgage Rates Affect Monthly Payments , you are in the right place. Let us demystify the math and look at how these numbers actually play out in the real world.

The Math of the “Tiny” Percentage | Why 1% is Actually a Fortune

Here is the thing about home loans: they are massive, long-term commitments. Because of this, even a microscopic change in your rate behaves like a snowball rolling down a hill. When you sign up for a mortgage, your payment is split into two primary components: principal and interest . The principal is the actual balance you borrowed; the interest is the fee the bank charges you to use their money.

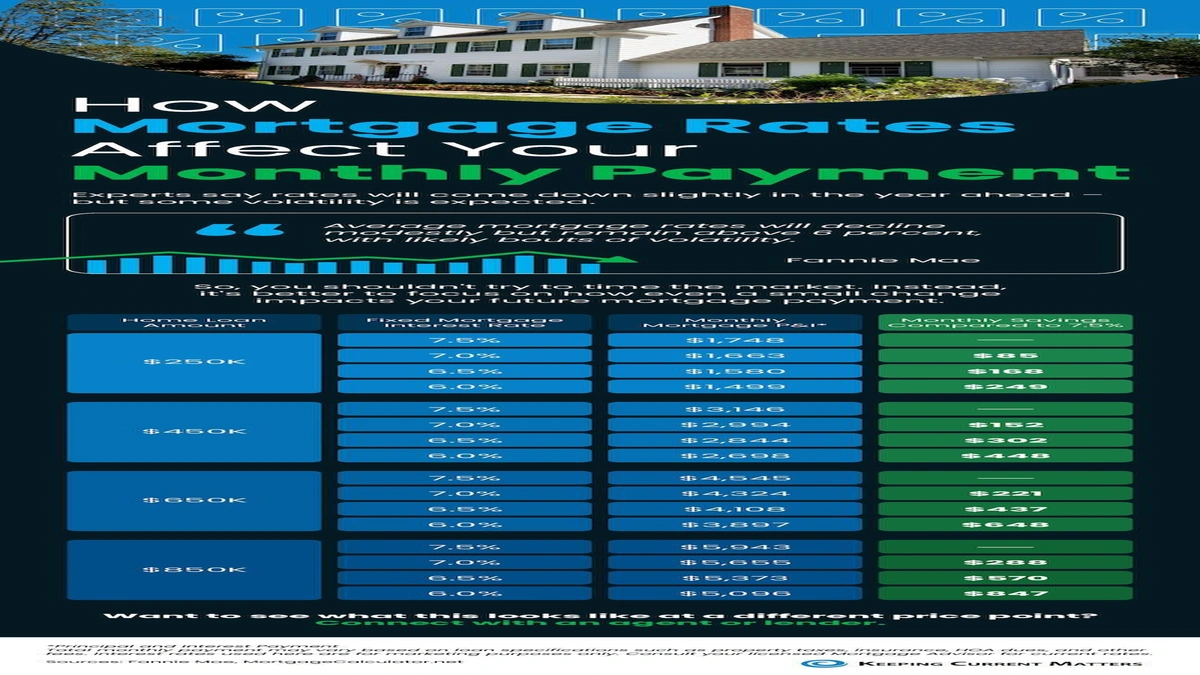

When interest rates climb, the portion of your payment dedicated to interest shoots up, while the principal portion remains unchanged. To see this in action, let us run some numbers. Suppose you take out a $400,000 30-year fixed-rate mortgage .

- At a 6% interest rate, your monthly principal and interest payment is approximately $2,398.

- If that rate climbs to 7%, your monthly payment jumps to roughly $2,661.

That is an extra $263 every single month. Over 30 years, that “insignificant” 1% difference translates to an extra $94,680 leaving your bank account. That is nearly a hundred thousand dollars that could have gone toward retirement, your children’s college fund, or family vacations. This is why keeping an eye on interest rate fluctuations is not just for Wall Street analysts it is a critical task for anyone looking to buy a home.

Inside the Amortization Black Box | Where Your Money Actually Goes

When you start paying off a home loan, you might assume that your monthly check is split evenly between paying off the house and paying off the bank. I initially thought this was straightforward, but then I realized the math is heavily stacked against you in the early years. This is dictated by something called an amortization schedule .

An amortization schedule is a table showing each periodic payment on an interest-bearing loan. In the beginning, the vast majority of your payment goes toward interest, not the principal. If you want to dive deeper into the technicalities of how banks structure these timelines, you can read more aboutmortgage loan structureson authority reference sites.

Because the interest is calculated based on your remaining loan balance, a higher mortgage rate means you build equity in your home at a agonizingly slower pace. Under a higher rate, it takes much longer for the scales to tip in favor of paying down the actual home balance. This is why understanding the relationship between rates and amortization is so critical before signing on the dotted line.

Choosing Your Weapon | Fixed-Rate vs. Adjustable-Rate Mortgages

When shopping for a loan, you will generally face two main pathways: a fixed-rate loan or an adjustable-rate mortgage (ARM). Each reacts very differently to market changes.

With a fixed-rate mortgage , your rate is locked in for the entire loan term (usually 15 or 30 years). Your monthly payment remains completely predictable. It is a safe harbor. Even if the economy goes wild and rates skyrocket, your payment does not budge.

On the flip side, an adjustable-rate mortgage usually offers a lower introductory rate for a set period (like 5 or 7 years), after which the rate adjusts periodically based on market index changes. While an ARM can save you money upfront, it exposes you to the winds of market changes. If rates rise, your monthly payment will rise with them sometimes dramatically. To model these different scenarios and see how they fit your budget, utilizing a reliable home loan EMI calculator is an absolute lifesaver. It takes the guesswork out of the math and lets you plan your financial future with confidence.

The Ripple Effect | Beyond Your Monthly Check

How do interest rates affect your broader financial picture? For starters, they directly dictate your buying power. Lenders assess your eligibility using your debt-to-income ratio (DTI), which is the percentage of your monthly gross income that goes toward paying debts.

When rates go up, your projected monthly payment increases. This higher payment might push your DTI past the lender’s comfort zone, meaning they will approve you for a much smaller loan amount. Suddenly, that 3-bedroom house you had your eye on is out of reach, and you have to adjust your expectations.

If you are trying to save up a larger down payment to offset these higher rates, you might be looking for ways to boost your income. Some people look into thebest work from home jobs no experienceto start bringing in extra cash to build up their savings. Alternatively, if you are a business owner aiming to optimize your business revenue to qualify for a better loan tier, adopting thebest free CRM software for small businesses to boost sales in 2026can make your company’s financials look incredibly robust to potential underwriters.

If you already own a home and are locked into a high rate, do not lose hope. You can always monitor the market for refinancing options . If rates drop significantly below what you are currently paying, refinancing can help you swap out your old loan for a new one with a lower rate, instantly slashing your monthly payment.

Frequently Asked Questions

How do I know if I should lock in my rate now?

If you are happy with the current rate and it fits your budget, locking it in is usually wise. Trying to time the market perfectly is incredibly difficult, and waiting for rates to drop further can backfire if they suddenly rise instead.

Does a higher credit score really lower my monthly payment?

Absolutely. Lenders offer their best, lowest interest rates to buyers with excellent credit scores. A lower rate directly translates to a lower monthly payment and less interest paid over the life of the loan.

What happens to my monthly payment if I make one extra payment a year?

While an extra payment won’t change your required monthly payment for the next month, it goes directly toward your principal balance. This reduces the total interest you owe and shortens the length of your loan significantly.

Can I negotiate my mortgage rate with my bank?

Yes, you can! You can shop around with different lenders, obtain multiple loan estimates, and ask your preferred bank to match the lowest offer you received. Even a fraction of a percent off can save you thousands.

How does the loan term affect the total interest I pay?

Shorter terms (like a 15-year mortgage) generally have lower interest rates and result in far less total interest paid over time, but your monthly payments will be significantly higher because you are paying off the principal much faster.

The Bottom Line

At the end of the day, mortgage rates are not just dry financial statistics. They are the unseen gears that determine the real-world cost of your home. A slight fluctuation can be the difference between easily making your payments each month and feeling stretched to your absolute limit. By understanding how these rates interact with your principal, amortization, and loan options, you put yourself firmly in the driver’s seat of your home-buying journey.